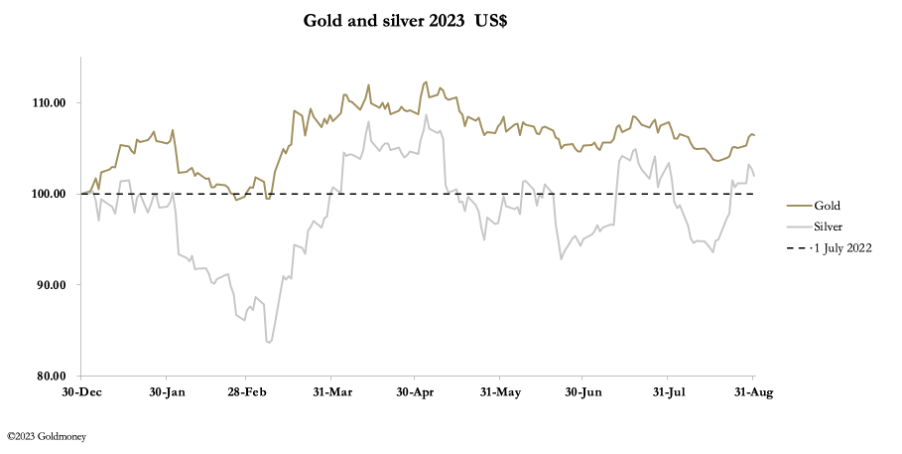

In the last few days, gold and silver have paused their earlier rises. In the case of silver, these have been substantial, as shown in our headline chart. In gold, less so; but it does appear that silver is leading both metals higher. In European trade this morning, gold was $1944, up $39 on the week, and silver $24.60, up 40 cents. Silver is up 10% from its mid-August low, leading gold which is up only 3%.

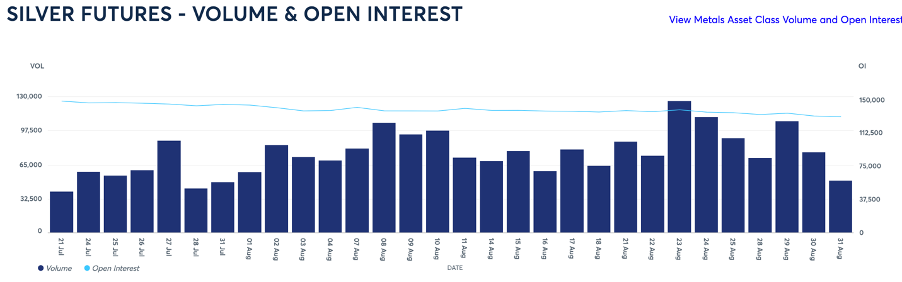

This performance has been despite Comex September contracts running off the board and the expiry of related options. And in silver, it is noticeable how Comex turnover has declined as it has consolidated, confirming that the next price move will almost certainly be higher. The screenshot below illustrates the position.

Silver’s outstanding performance in late-August can be attributed to a bear squeeze, with the hedge funds having been net short 6,670 contracts on 15 August. The last Commitment of Traders figures (22 August) show them squeezed into net long 1,383 contracts. Meanwhile, the Swaps (mainly bullion bank traders) maintained a net long position of 5,978 and 5,856 contracts respectively. The bear squeeze is on the speculators, while the establishment is trying to maintain a modest long position.

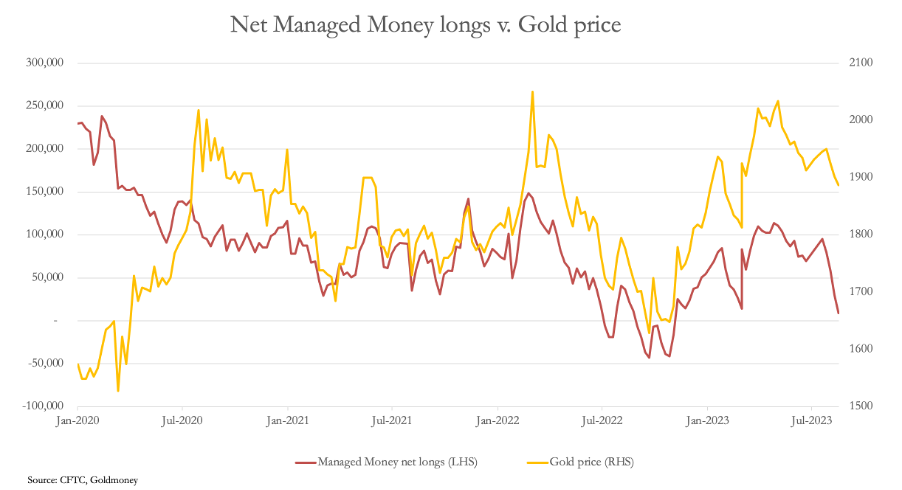

A similar condition exists in the gold contract, with the net long position for the Managed Money category having fallen to 9,109 contracts on 22 August. This is exceptionally low, as illustrated next.

It is notable that from the gold price peak in August 2020 the net longs have correlated with the price. What this means is that the hedge fund cohort is always long at the top and least so at the bottom. They seem to behave like gambling addicts in a betting shop, proving that other macro information is no guide for them.

Their principal macro guides are US interest rates and the dollar’s trade weighted index. In recent days, the yield on the 10-year US Treasury and the TWI have eased slightly, as the next charts of their performance last month shows.

There is little doubt that the easing of bond yields does take stress off the financial system. It is good for financial asset values generally, and it takes some pressure off bank balance sheets, whose mark-to-market losses on securities are estimated to be $620bn by Nouriel Roubini, the economist who accurately predicted the 2008 banking crisis. But to these losses, says Roubini, should be added the fall in the value of mortgages on their books, giving an overall loss of $1.8 trillion, compared with equity capital for the entire banking sector of about $2.3 trillion.

Undoubtedly, there are further problems in the regional banks, likely to be exposed by the developing credit crunch, as the better capitalised banks refuse to recycle credit through interbank markets. It might not even need a further rise in interest rates or bond yields to trigger the next bank failure.

Whither gold and silver prices then? Hedge funds are likely to be wrong-footed again.

Source link