Turned upside-down since late 2008 with QE and interest rate repression, it still hasn’t been turned right-side up.

By Wolf Richter for WOLF STREET.

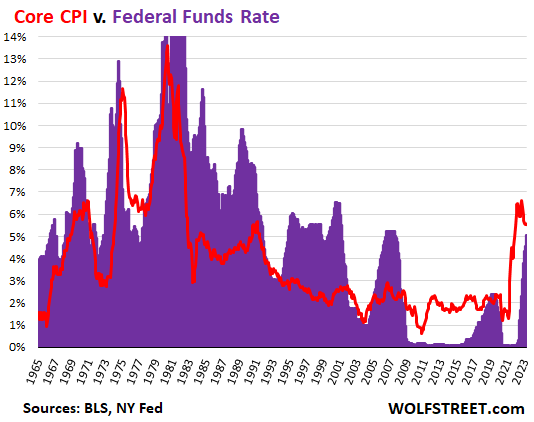

The Fed has now raised its policy rates by 500 basis points in a little over a year, with the top of the range now at 5.25%, and with the Effective Federal Funds Rate at 5.08%. But “core” CPI, which excludes the volatile food and energy components, has gotten stuck at around 5.5% to 5.7% for the fifth month in a row. There wasn’t any progress at all with core CPI in five months. Inflation intensity is simply shifting from one category to another. As inflation temporarily subsides in one category, it resurges in another.

The Fed’s short-term policy rate, as measured by the Effective Federal Funds Rate (purple), is still below inflation, as measured by core CPI (red):

With core CPI at 5.52% in April, the “real” Effective Federal Funds Rate (EFFR minus core CPI) is still a negative 0.44%. And negative real policy rates are still a form of interest rate repression, and are still stimulative of the economy and of inflation.

And so core CPI got stuck at 5.5% to 5.7%, and isn’t making any efforts to be heading toward 2% or whatever, and instead, everyone has gotten used to this inflation and accepts it, and deals with it, and builds it into economic decisions, which is nurturing this inflation right along.

In other words, with its current policy rates, the Fed is still just removing accommodation, rather than turning the screws on inflation.

But the crybabies on Wall Street are out there in force screaming about those unfair interest rates and clamoring for immediate rate cuts, like in June, to remove this incredible injustice of 5% short-term rates and even lower long-term Treasury yields (the 10-year Treasury yield is at 3.43%, LOL), when core CPI is 5.5%.

For those crybabies on Wall Street, the best money is free money. They want their 0% back, and they want their QE back. But now we have this inflation that’s not going away.

When we look back 60 years, we see what an extraordinary period this QE and interest rate repression since 2008 has been. During almost the entire 14 years — except for a few months in 2019 — the Fed’s policy rate was far below the rate of core CPI. And to this day, it remains below core CPI. But that’s an upside-down version of what was the rule before 2008.

The chart below goes back to 1965. Before 2008, the rule was that the Fed’s policy rates were nearly always higher or substantially higher than the rate of inflation. For example, in the 1990s, the EFFR was around 5% to 6%, while core CPI was around 2% to 3%. In other words, the EFFR was double the rate of inflation, which is what pushed down inflation. And those were booming times. I mean, we even had the magnificent Dotcom bubble.

Over those decades from 2008 back to 1965, there were only a few relatively brief periods when the Fed’s interest rates were below the rate of inflation as measured by core CPI.

But since late 2008, we’ve had the opposite. Policy was turned upside down. And it still hasn’t been turned right-side up. There is still a ways to go. And just looking at this chart, I get the distinct feeling that inflation is just being fueled further, rather than being doused, by the Fed’s current interest rates:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Source link