Timing the gold market is one of the most common concerns for new and experienced buyers alike. When the gold price is rising, it feels like you have missed the opportunity. When it falls, it feels like it might fall further. The result, for many people, is waiting indefinitely for a moment that never quite feels right.

The honest answer is that gold’s long-term track record makes the timing question less important than it first appears. Over decades, gold has preserved wealth through inflation, currency crises, and periods of economic uncertainty that no buyer could have predicted in advance. Investors who bought at what felt like the wrong time have generally been rewarded for patience. That does not mean timing is irrelevant, but it does mean that for most long-term buyers, the best time to buy gold is often simply when they are ready to do so.

That said, there are frameworks for thinking about entry points — seasonal patterns, macroeconomic signals, and strategies like dollar-cost averaging — that can help buyers feel more confident in their decision. This guide covers all of them: the case for buying now, historical timing patterns, and the factors that tend to drive the gold price, so you can make the decision that is right for you.

Is Now a Good Time to Buy Gold?

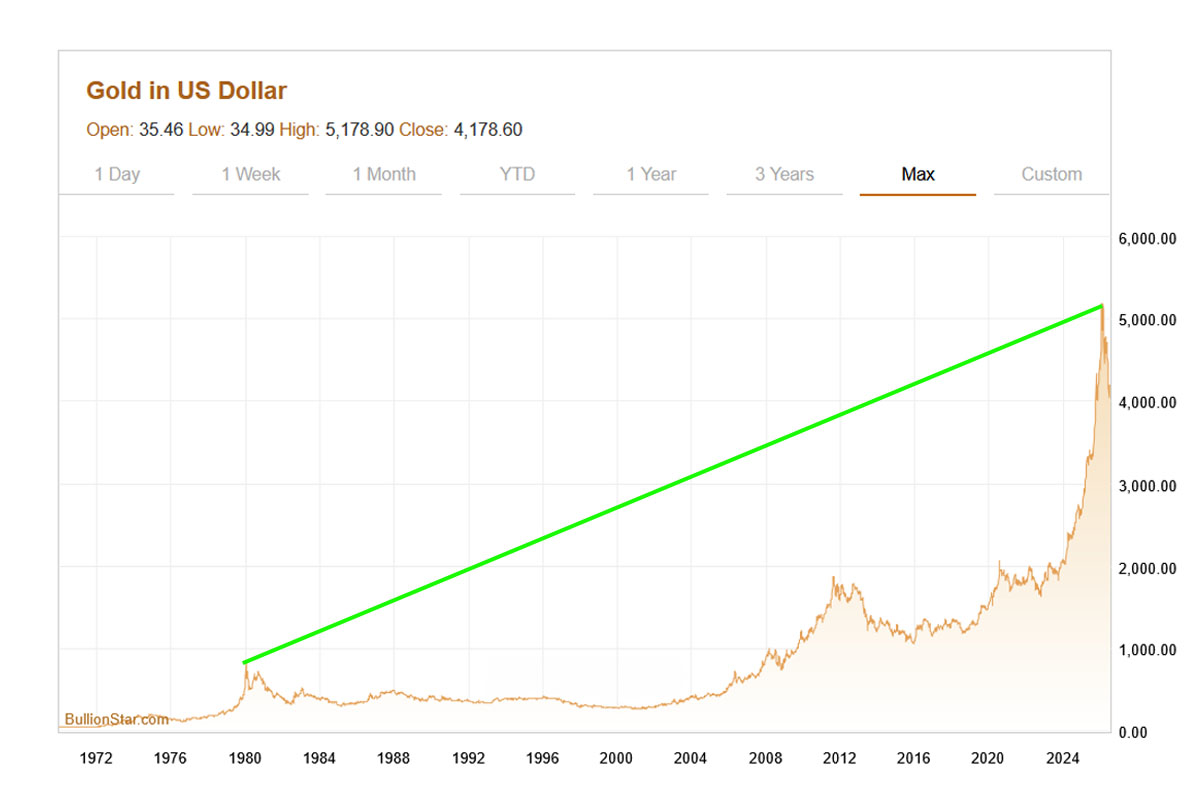

Gold is currently trading at around US$4,000 per troy ounce, up approximately 20% over the past twelve months. Analyst sentiment heading into 2027 remains broadly bullish, with central bank demand, dollar weakness, and geopolitical uncertainty cited as the primary drivers.

For a full breakdown of where major banks and institutional analysts expect the gold price to go, see our Gold Price Forecast 2027.

Whether that represents a good entry point depends on what you are buying gold for. Investors watching the price from the sidelines, waiting for a meaningful pullback, often find that dips are smaller and shorter than expected — and that the price has moved higher again by the time they feel comfortable acting.

Is It a Good Time to Buy Gold?

For most buyers with a long-term investment horizon, yes.

The case for buying now rests on gold’s role as a long-term store of value rather than a short-term trade. The factors that have supported gold over decades (inflation risk, currency debasement, geopolitical instability, and central bank demand), have not diminished. Buyers who have entered at various points over the past twenty years, including at prices that felt high at the time, have in most cases seen their holding appreciate over a long enough horizon.

The case for waiting exists, but is more difficult to justify. If you believe a significant price correction is likely in the near term, or if you plan to invest a larger sum, spreading purchases over time through dollar-cost averaging can reduce the impact of short-term volatility. We cover that approach in more detail in the timing frameworks section below.

The more useful question for most buyers is not whether now is a good time to buy gold, but whether their reasons for doing so are sound. Gold has historically rewarded patience. Investors who have entered at prices that felt elevated at the time have, over a long enough horizon, generally seen their holding appreciate. Those who waited for the perfect moment have often waited too long, paying more for their gold, or accumulating at a slower pace than they intend.

When to Buy Gold: Timing Frameworks

For buyers who want to think more carefully about their entry point, there are a handful of frameworks that can help structure the decision. None of them guarantee you will buy at the lowest possible price (no approach does) but they offer a more disciplined alternative to acting on instinct or waiting indefinitely.

Dollar-Cost Averaging

Dollar-cost averaging (DCA) means buying a fixed amount of gold at regular intervals (monthly, quarterly, or on whatever schedule suits your budget), regardless of the current price. When the price is high, your fixed amount buys less gold. When the price is lower, it buys more. Over time, this averages out your cost per ounce and removes the pressure of trying to time the market.

For most long-term buyers, DCA is the most practical approach. It is straightforward to maintain, removes emotion from the decision, and means you are never fully exposed to having committed everything at an unfortunate moment. BullionStar’s AutoInvest feature is designed specifically for this — allowing you to set up automatic recurring purchases on your preferred schedule.

Lump Sum Buying

A lump sum purchase — buying your full intended amount in one transaction — makes sense when you have a strong view that conditions favour gold, or when you simply want to establish a position and hold it without ongoing decisions. Historically, lump sum investing has outperformed DCA in rising markets, because more capital is deployed earlier. In a gold market that has trended upward over decades, that logic has generally held.

The trade-off is psychological as much as financial. A lump sum buyer who enters just before a short-term correction faces an on-paper loss immediately, which can be uncomfortable even for investors who understand the long-term picture. For buyers who are confident in their outlook and can hold through volatility, a lump sum is a perfectly rational approach. For those who are less certain, or buying a meaningful sum for the first time, DCA reduces that risk.

Dollar-Cost Averaging

Lump Sum

Best for

First-time buyers; larger sums; uncertain markets

Confident buyers with a clear view; smaller sums

Price exposure

Averaged over time

Full exposure at point of purchase

Effort

Ongoing commitment required

Single decision

Performance in rising markets

May lag — later purchases cost more

Stronger — more capital deployed earlier

Performance in falling markets

More resilient — later purchases cost less

Full position exposed to drawdown

Emotional difficulty

Lower

Higher

Suited to

Long-term wealth building

Establishing a position quickly

Buying on Price Dips

Waiting for the gold price to drop before buying is a natural instinct, and there is nothing wrong with being patient if you believe a correction is coming. Gold does experience pullbacks and buying into weakness rather than strength can improve your entry price.

The challenge is that gold price drops are difficult to predict and often short-lived. The gold price does not follow a reliable cycle that makes dips easy to anticipate, and waiting for a correction that does not come, or that recovers quickly, can mean missing a sustained upward move. If you plan to buy on dips, having a price level or percentage pullback in mind before you start watching is more disciplined than reacting to daily movements.

The Gold-to-Silver Ratio

The gold-to-silver ratio measures how many ounces of silver it takes to buy one ounce of gold. Historically, the ratio has ranged widely, from a modern low of around 17 in 1980 to above 120 during the Covid-19 panic in 2020. Some investors use it as a relative value signal for timing their precious metals purchases.

When the ratio is historically high, silver is considered cheap relative to gold, and some investors shift allocation toward silver. When the ratio is low, gold is considered relatively more attractive. For gold buyers specifically, a very high ratio can suggest that gold is priced at a premium relative to its historical relationship with silver — a signal that some use to favour silver or wait before adding to gold.

The ratio is a useful contextual tool, but it works best as one input among several rather than a standalone timing signal. Ratios can remain at extremes for extended periods, and the relationship between gold and silver is influenced by industrial demand for silver as well as investor sentiment — making direct comparisons imperfect.

For a full breakdown of the gold-to-silver ratio, its historical context, and how investors use it in practice, see our Gold Silver Ratio: A Complete Guide.

Best Month and Day to Buy Gold

Gold does not move in perfectly predictable cycles, and can be influenced by unexpected events, but historical price data does show some consistent seasonal tendencies. For buyers who have flexibility over when to act, understanding these patterns can be a useful secondary consideration — though they should inform rather than dictate a buying decision.

Gold Price Seasonality: Best Month to Buy Gold

Analysed across decades of price data, gold tends to follow a broadly consistent seasonal pattern. Prices are typically softer during the spring and early summer months, with March through July historically showing the weakest average performance of the year. This period often coincides with lower jewellery demand globally and a quieter phase in institutional buying.

From late summer onward, the picture typically strengthens. August and September have historically seen gold begin to recover, driven in part by the start of the Indian wedding and festival season, which generates significant physical gold demand across South and Southeast Asia. That demand tends to carry through into the fourth quarter, with the Diwali and Christmas periods both associated with elevated gold buying. January and February also tend to be firmer, partly reflecting renewed institutional positioning at the start of the year.

The table below summarises the historical seasonal tendencies by month:

Month

Typical Tendency

Key Driver

January

Firm

Institutional positioning; carry-over demand

February

Firm

Valentine’s Day jewellery demand

March

Softening

Seasonal lull begins

April

Soft

Lower demand period

May

Soft

Lower demand period

June

Soft

Typically weakest stretch of the year

July

Soft / Turning

Demand beginning to recover

August

Recovering

Indian festival season begins

September

Firmer

Navratri; renewed institutional interest

October

Firm

Diwali demand

November

Firm

Post-Diwali; year-end buying

December

Variable

Christmas jewellery demand; year-end profit-taking

These are tendencies based on historical averages, not guarantees. Any given year can diverge significantly from the seasonal pattern depending on macroeconomic conditions, geopolitical events, or sudden shifts in investor sentiment.

Best Day to Buy Gold

Within any given week, gold price data shows that Tuesday and Wednesday have historically tended to be the weakest days for the gold price. Monday often sees some upward pressure as markets reprice over the weekend’s news, while Thursday and Friday can see positioning ahead of the weekly close. Mid-week, when that initial momentum has settled and end-of-week activity has not yet begun, prices have historically been marginally softer on average.

As with seasonal patterns, the differences between days are modest and easily outweighed by broader market movements. Trying to time a purchase to a specific day of the week is unlikely to make a meaningful difference to your long-term return. For buyers making a one-off purchase, a Tuesday or Wednesday is a reasonable default if you have flexibility. For buyers using dollar-cost averaging, the day of the week is largely irrelevant — consistency matters more than precision.

Gold Price Drivers and Trend Indicators

Understanding what moves the price of gold can help you make a more informed decision about when to buy — not by predicting the market, but by recognising the conditions that have historically supported gold’s value.

The key drivers are well established: US interest rates and real yields, US dollar strength, inflation expectations, central bank demand, and geopolitical risk. These factors do not move in isolation, and their combined effect on the gold price at any given moment is rarely straightforward. A rising gold price during a period of high interest rates, for example, may reflect geopolitical demand outweighing the traditional headwind from yields.

For buyers thinking about timing, the most practical takeaway is this: conditions that are broadly negative for the dollar and equities have historically been positive for gold. When those conditions are present — elevated inflation, economic uncertainty, dollar weakness — gold’s case as a store of value strengthens. When financial conditions are stable and real yields are positive, gold faces more headwinds, though it has still proven capable of performing well in those environments over longer horizons.

For a full breakdown of the macroeconomic factors that drive the gold price, visit our dedicated guide: What Drives Gold and Silver Prices? Key Macroeconomic Factors to Watch.

Frequently Asked Questions

Should I wait for gold to drop before buying?

Waiting for a lower entry point is a natural instinct, but it carries a real risk: the drop may not come, or may be shorter and smaller than expected. Gold has spent most of the past two decades trending upward, and buyers who have waited for a significant correction have often found themselves buying later at a higher price than they would have paid by acting sooner. If you are waiting indefinitely for the right moment, dollar-cost averaging is likely to serve you better.

Is dollar-cost averaging good for gold?

Yes, for most long-term buyers, dollar-cost averaging is a practical approach to building a gold position. By buying a fixed amount at regular intervals, you automatically acquire more gold when prices are lower and less when they are higher, averaging out your cost per ounce over time. It also removes the pressure of timing the market entirely, which for most investors is a significant psychological benefit. BullionStar’s AutoInvest feature is designed specifically for this, allowing you to set up automatic recurring purchases on your preferred schedule.

Are there bad times to buy gold?

From a long-term perspective, there are very few genuinely bad times to buy gold. Buyers who entered at prices that felt high at the time have generally been rewarded over a long enough horizon. Short-term, there are conditions that create headwinds for gold, but these tend to be transitory rather than permanent. The more relevant question for most buyers is not whether now is a bad time, but whether they are buying for the right reasons and with a realistic time horizon.

Does gold always go up long-term?

Yes, but not in a straight line, and there can be periods of consolidation or decline. Gold fell through the 1980s and 1990s after its 1980 peak, and experienced a pullback after its 2011 high. What gold has demonstrated over the very long term is a strong tendency to preserve purchasing power — outpacing inflation and maintaining value relative to fiat currencies over decades. Investors with a long time horizon and realistic expectations have historically been well served.

Is the gold price falling?

Despite strong performance over the past year, gold is currently trading at approximately $4,000 per ounce, down 10% over the past three months, due to expectations for higher interest rates. Short-term price movements in gold are driven by a combination of factors — dollar strength, interest rate expectations, geopolitical developments — and can shift quickly. For long-term buyers, short-term price direction is less relevant than the underlying conditions that support gold’s value over time. If you are concerned about near-term volatility, dollar-cost averaging reduces your exposure to any single entry point.

When does the gold price drop?

Gold price drops are not reliably predictable, but historical patterns offer some guidance. Seasonally, gold has tended to be softer between March and July, when jewellery demand is lower and institutional activity quieter. More significant corrections have typically coincided with periods of dollar strength, rising real yields, or sharp recoveries in risk assets — conditions where investors move out of safe havens.

When Is the Best Time to Buy Gold? Key Takeaways

The honest answer to the question this page set out to address is that for most long-term buyers, the best time to buy gold is when they are ready to do so. The seasonal patterns, timing frameworks, and market indicators covered in this guide are useful tools for making a more informed decision — but none of them are more important than having a clear reason for buying and a realistic time horizon for holding.

Gold has rewarded patience consistently over the long term. Buyers who entered at prices that felt high have generally fared well over years and decades. The investors who have struggled are more often those who waited too long for a perfect entry point that never came, or who bought with a short-term mindset and sold during temporary corrections.

BullionStar makes it straightforward to start buying gold on your own terms — whether that is a one-off purchase, a regular AutoInvest plan, or physical gold held in secure vault storage. Browse our full range of gold bullion, or visit our Bullion Center at 45 New Bridge Road, Singapore. If you have any questions, our team is available at [email protected].

Source link