This analysis focuses on gold and silver within the Comex/CME futures exchange. See the article What is the Comex? for more detail. The charts and tables below specifically analyze the physical stock/inventory data at the Comex to show the physical movement of metal into and out of Comex vaults.

Registered = Warrant assigned and can be used for Comex delivery, Eligible = No warrant attached – owner has not made it available for delivery.

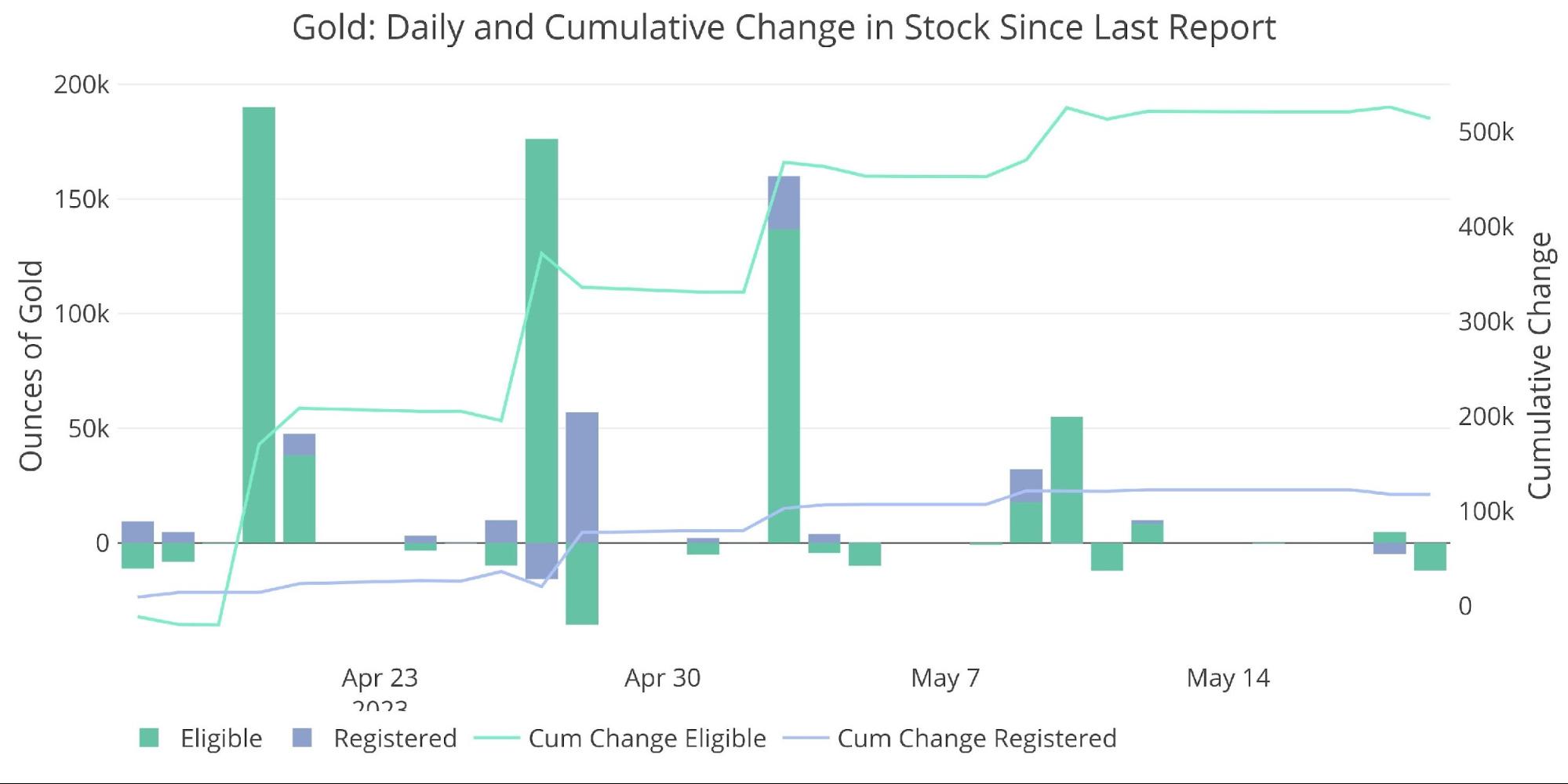

Gold

Banks continue to add metal back to their vault after seeing 11 months of new outflows. Since mid-March, banks have added 1.3M ounces of gold to their inventories.

Figure: 1 Recent Monthly Stock Change

The daily activity can be seen below and looks very strategic. JP Morgan made big moves in March moving almost their entire Eligible stack to Registered. Since then, JP Morgan has been adding strategically. The green bars below are primarily driven by JP. adding 150k-190k ounces per week for three weeks. The latest week did not show a big add, signaling JP may be done adding. Since mid-March, they have added a net 1.19M ounces.

Figure: 2 Recent Monthly Stock Change

Pledged gold saw a brief uptick, but most of that seems to have dissipated.

Figure: 3 Gold Pledged Holdings

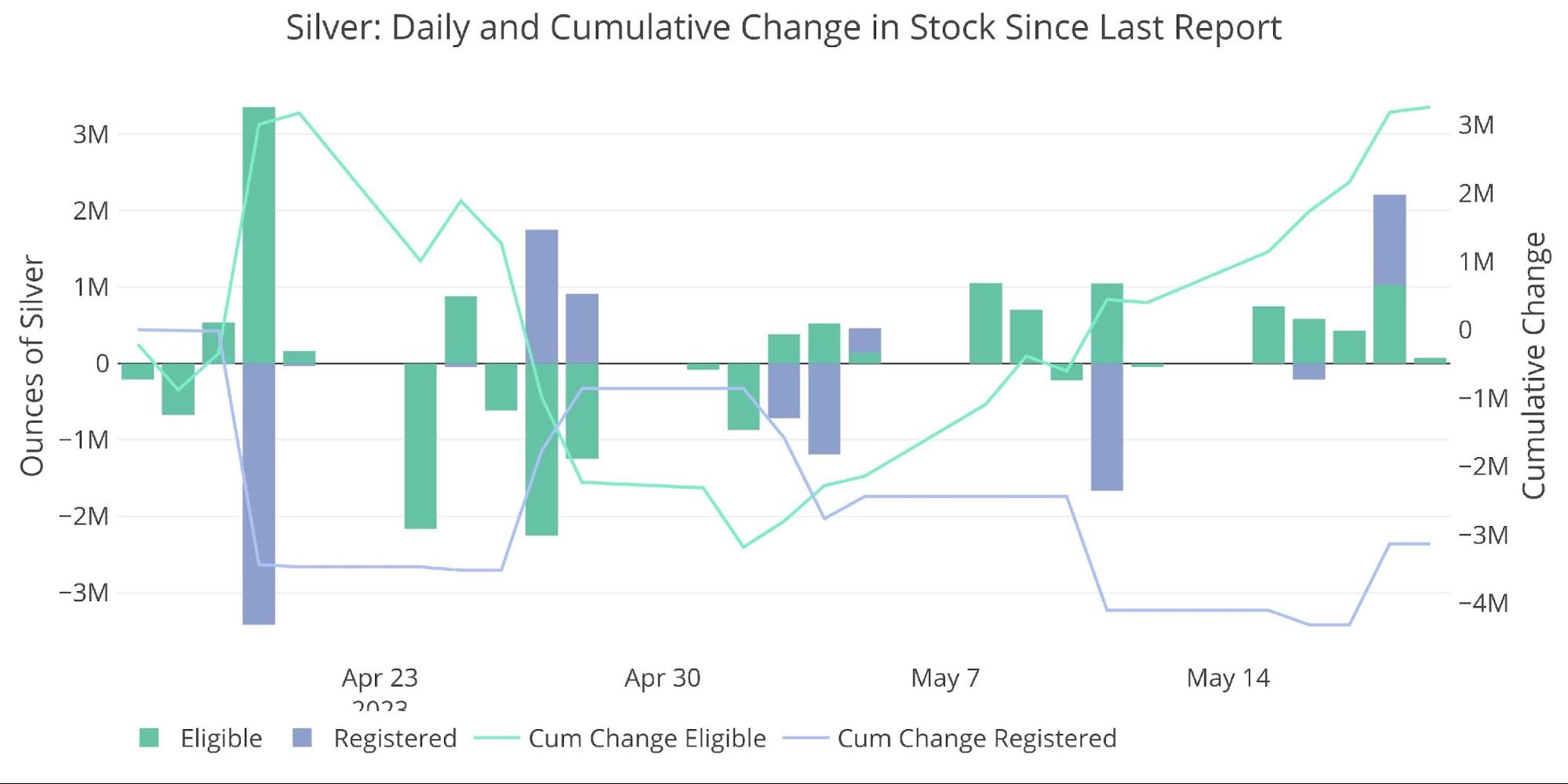

Silver

Banks have also restocked silver. In May alone, banks have added a net 3.2M ounces. This has been in Eligible as Registered has continued to drop, falling 2.27M ounces since May 1st.

Figure: 4 Recent Monthly Stock Change

The daily activity shows most of that inventory drop for Registered occurred back in late April. Thursday actually saw 1.18M ounces enter the vault, possibly to prepare for the upcoming minor delivery month in silver (more on this next week).

Figure: 5 Recent Monthly Stock Change

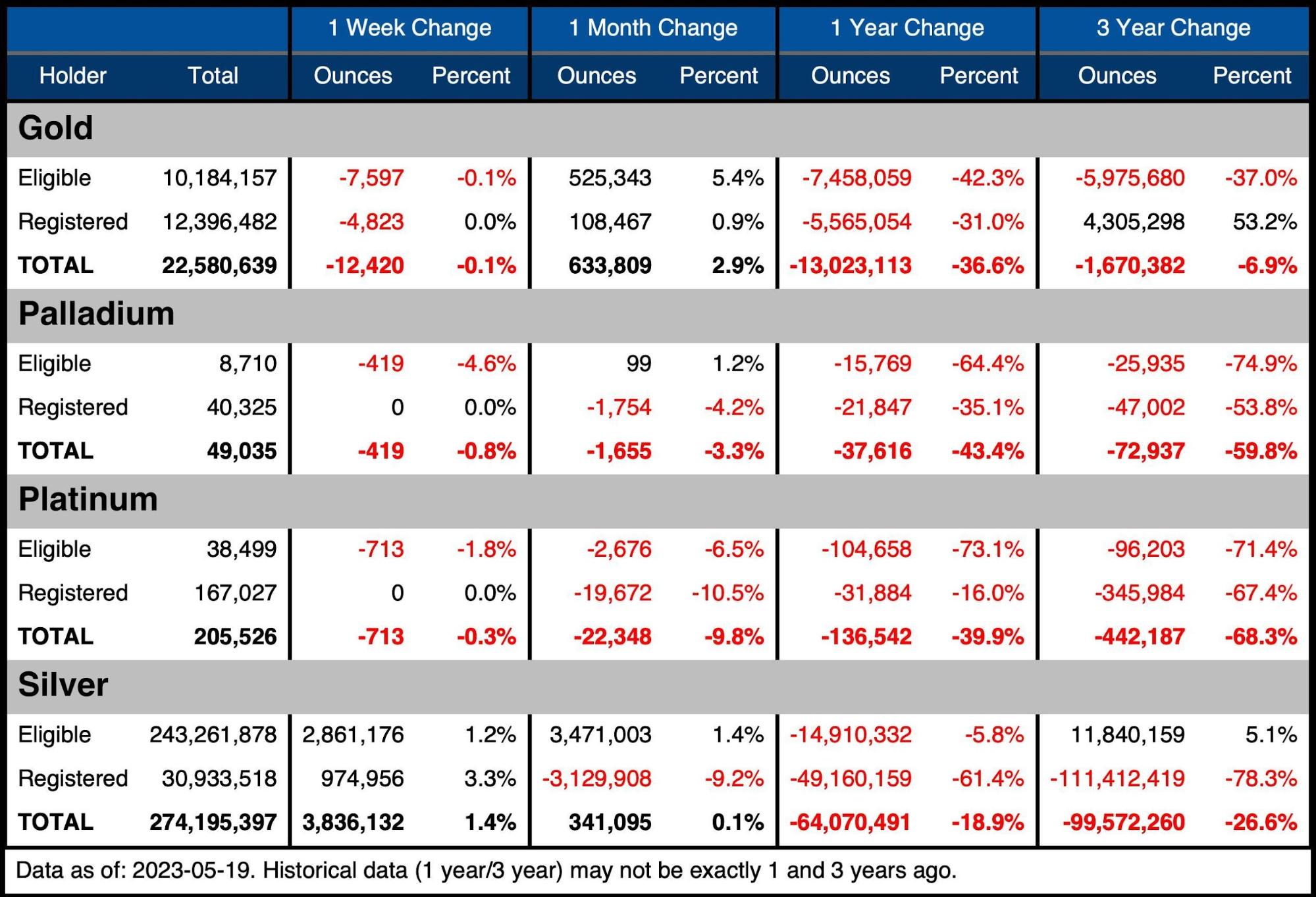

The table below summarizes the movement activity over several time periods to better demonstrate the magnitude of the current move.

Gold

Net inflows increased vault totals by 2.9% over the month

Inventories are still down 36% since last year, tilted slightly toward Eligible

The latest week saw modest net outflows

Silver

Silver saw a big move this week, adding 3.8M ounces

Over the month, total inventories are pretty flat

Registered declined 9% while Eligible increased 1.4%

Palladium/Platinum

Palladium and platinum are much smaller markets but it’s possible that is where the market breaks first.

Both metals have seen small net outflows. This could be a factor over the next two months with both metals seeing strong open interest in their respective contracts (more details next week)

Figure: 6 Stock Change Summary

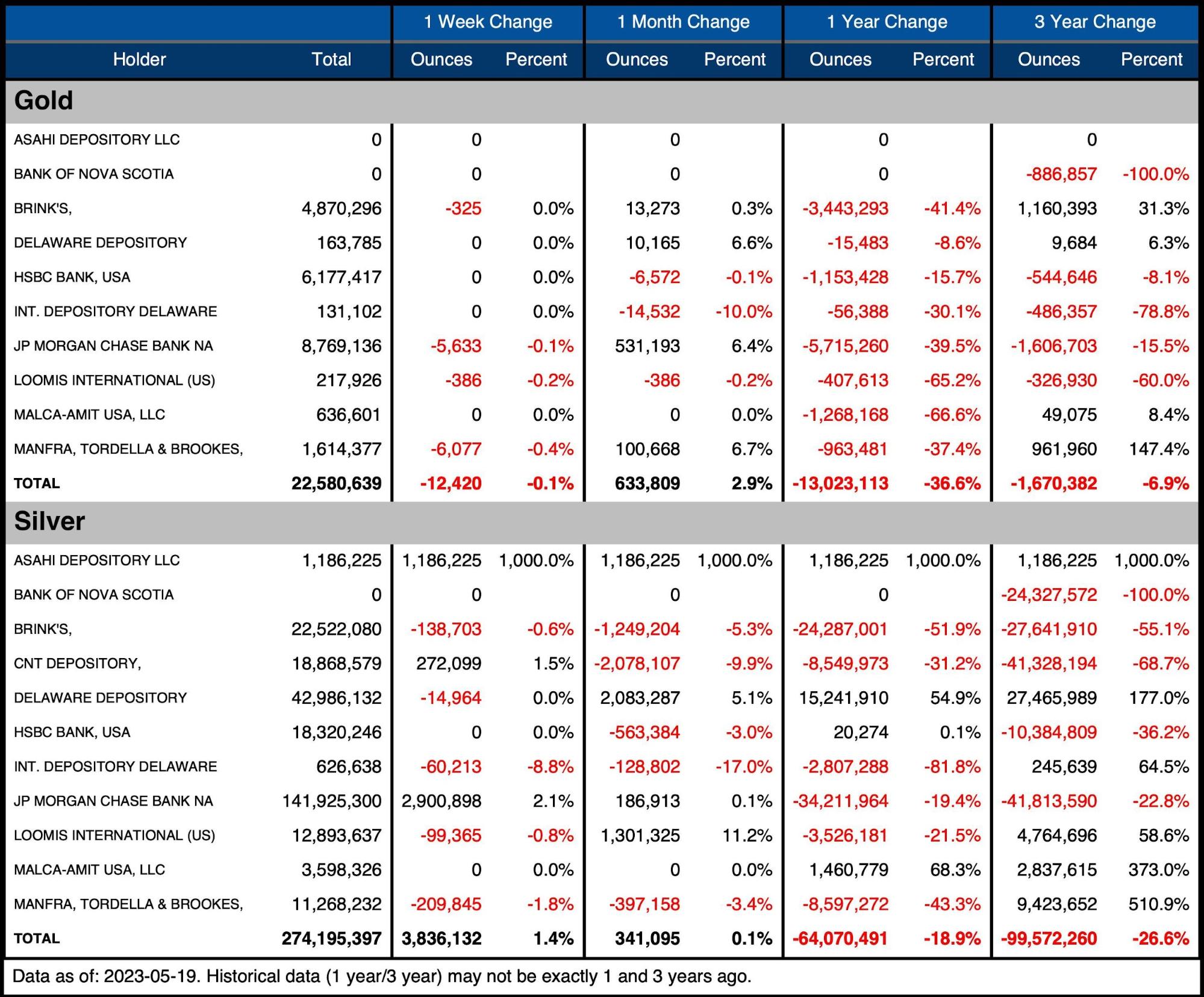

The next table shows the activity by bank/holder. It details the numbers above to see the movement specific to vaults.

Gold

With the addition of 531k ounces, JP has now increased inventories by over 1M ounces over the last 60 days

Other banks sow some modest increases over the last month, but only outflows over the last week

Silver

Delaware and Loomis were the players adding this month.

A new depository has arrived (Asahi) and saw an initial deposit of 1.2M ounces

JP Morgan saw a very modest increase in inventories over the month, but considering the 2.9M increase this week, the month balance had been negative by 2.8M ounces

Figure: 7 Stock Change Detail

Historical Perspective

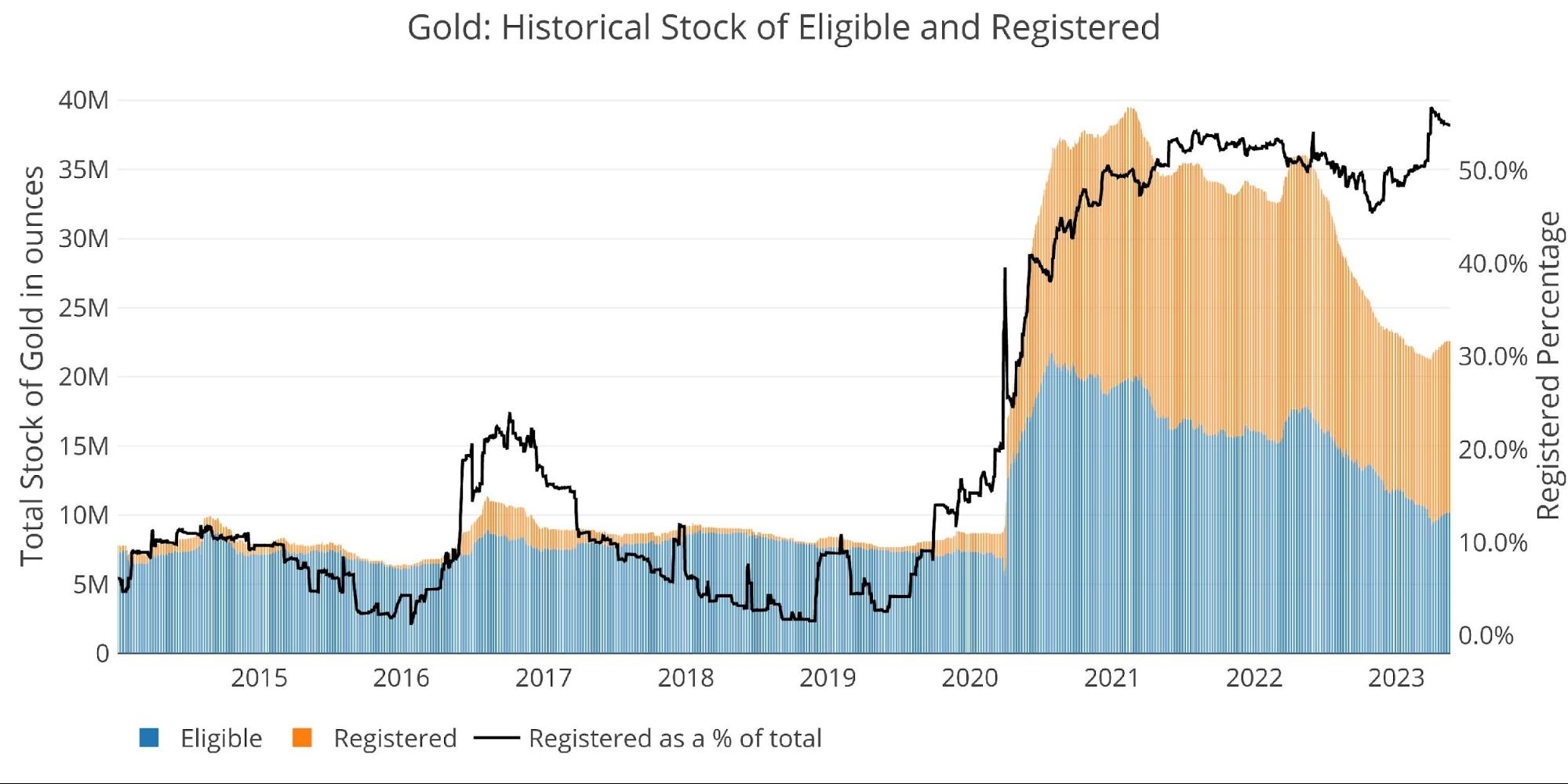

The recent activity in gold can be put into context by the chart below. Have banks restocked in the last month? Yes. Is it noticeable? Yes. Does it move the needle? No. The last year has seen such a massive drawdown in inventories that the recent increase by banks has done little to actually replenish those supplies.

Personally, I think the move by JP Morgan over the last two months was done to replenish dangerously low supplies. The data and activity suggest that the actual supply of gold is much smaller than what is shown as available below. This is primarily because the supply boost in 2020 may have been more for confidence than an actual surge in physically available metal.

Figure: 8 Historical Eligible and Registered

The drawdown in silver has been more concentrated in Registered. This has brought the ratio of Registered to total silver supplies to 11% which is the lowest on record.

Figure: 9 Historical Eligible and Registered

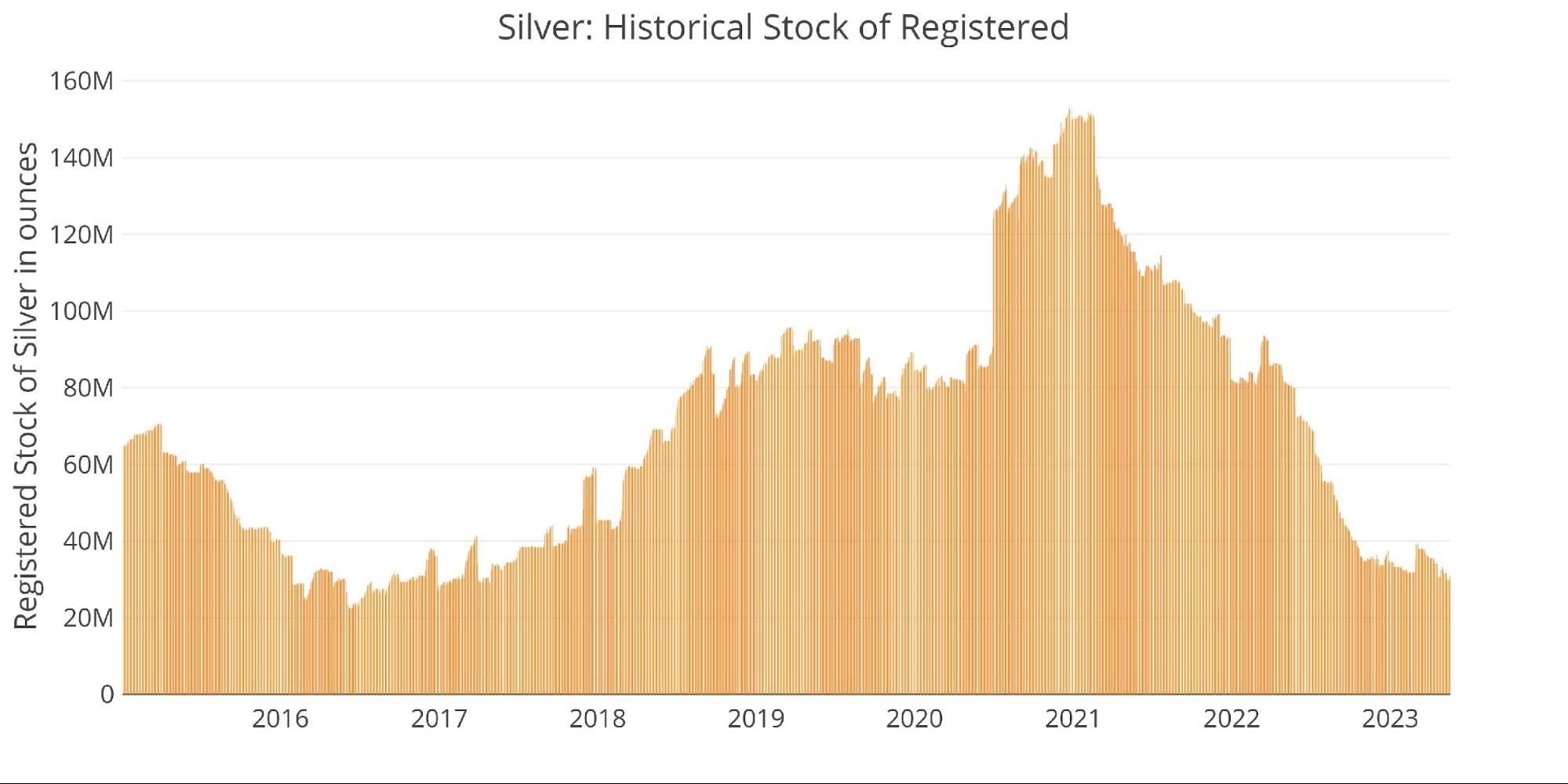

Below shows just the Registered component. The recent mini spike occurred just as the March delivery contract started. It has been entirely undone over the last two months, falling below 30M ounces before the increase on Friday that brought stocks above 30M. The Comex has seemed to want to keep total Registered above 30M ounces, again this could potentially be to keep confidence in the market, while real supplies available are far less than 30M ounces.

Figure: 10 Historical Registered

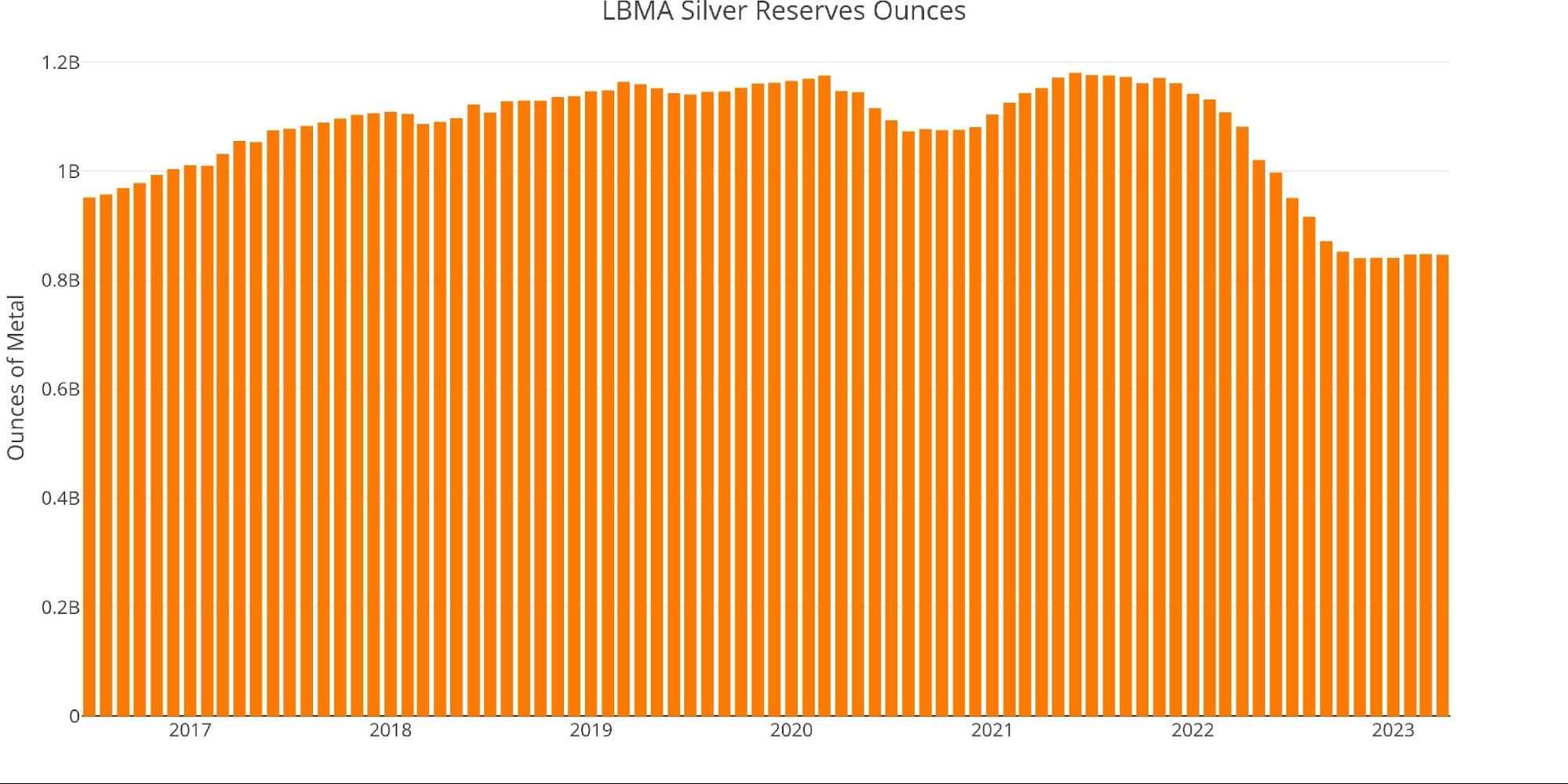

The LBMA had been seeing similar outflows of silver from their vault, which has slowed over the last few months though. There was a slight downtick of 2M ounces in the latest month.

Figure: 11 LBMA Holdings of Silver

Available supply for potential demand

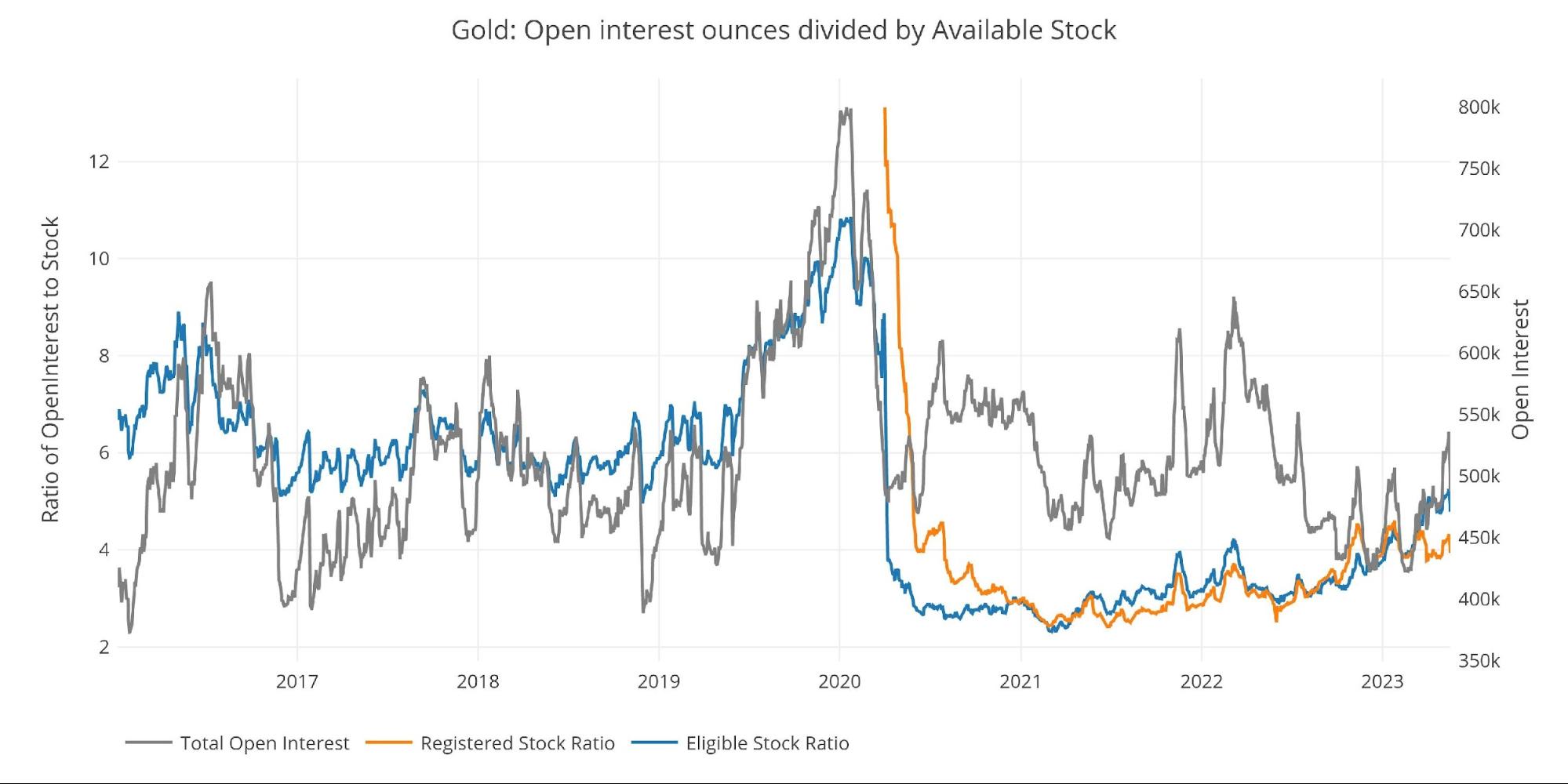

Before the recent sell-off in gold, open interest reached 536k contracts on May 15th. This means there were 4.3 paper contracts for each ounce of Registered gold at the Comex. The high since the Covid supply restocking was 4.5 in November, which means current inventories remain very low despite the recent restocking.

Figure: 12 Open Interest/Stock Ratio

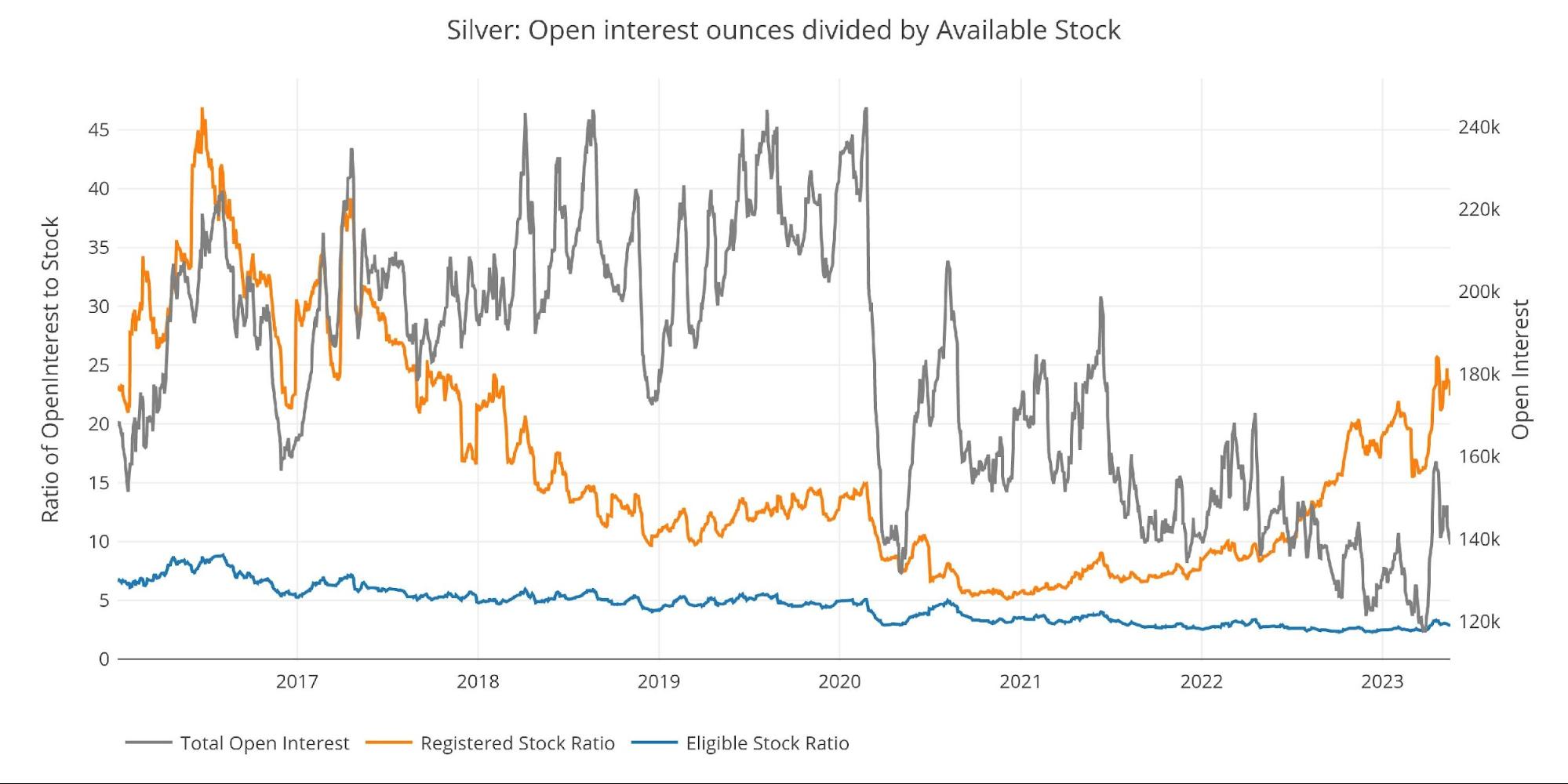

Coverage in Registered silver is far worse than gold and reached a new low for the move of 25.6 back in April. The recent sell-off in silver was caused by a big drop in open interest. This has brought the ratio down to 22.4. While that is an improvement, it still means that there are more than 22 paper ounces for each physical ounce of silver at the Comex. If 5% of contract holders stood for delivery, then the Comex would be wiped out of supply.

Figure: 13 Open Interest/Stock Ratio

Wrapping Up

The banks have restocked over the last month, but the charts put this move into context and show how much supplies have been depleted recently. The slow drain on the Comex continues. If anything, the current restocking could be more evidence that actual supplies are way lower than what is shown in the daily Comex reports.

Are all 30M ounces of Registered silver actually available for delivery? Probably not. So where is the actual bottom? The Comex seems intent on keeping a floor of 30M ounces, so perhaps that is very near the bottom. The outflows have slowed some, but as turmoil picks up with higher interest rates, and more countries move to de-dollarize, the demand for physical will only grow. The recent restocking by banks will likely be undone quickly.

Data Source: https://www.cmegroup.com/

Data Updated: Daily around 3PM Eastern

Last Updated: May 19, 2023

Gold and Silver interactive charts and graphs can always be found on the Exploring Finance dashboard: https://exploringfinance.shinyapps.io/goldsilver/

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Source link