By Alasdair Macleod

Increasing numbers of national governments are abandoning the US sphere of influence. Opportunities from trade with Asia compare favourably with rising currency and banking risks in a dollar-centric world.

Against an imploding banking system in long-established financial markets, China’s renminbi looks like a safe haven. Thanks to a savings-driven economy, China’s consumer price inflation remained very low, when those of the western alliance soared.

Now we face a credit crunch, as banks struggle to reduce their operational gearing which has become uncomfortably high. Consequently, borrowing rates will be driven higher, taking interest rate control out of central banking hands. Higher interest rates and therefore bond yields due to a credit crunch will escalate the banking crisis, which is only in its early stages.

Consequently, central bank credit will be inflated to prevent the commercial banking network from collapsing and to fund rising government budget deficits. It is the prospect and realisation of these conditions which will lead ultimately to a collapse of fiat currency values, and foreign holders of dollars, euros and sterling are only beginning to understand the danger.

Geopolitics are now undermining the dollar

In recent weeks, the threat to the dollar’s hegemony has noticeably increased. Like rats deserting a sinking ship, growing numbers of countries are backing off from the dollar in favour of China’s renminbi, and to a lesser extent other emerging market currencies. China has brokered a peace deal between Iran and Saudi Arabia, and in turn the Saudis are now improving their diplomatic relations with Syria.

It appears that America’s divide-and-rule Middle East policy has been overthrown. Even Mexico is reported to be prepared to accept renminbi in defiance of its northern neighbour’s policies. And Brazil has always been the B in BRICS. Now Argentina has applied to join an expanding BRICS, alongside Algeria, Indonesia, and Iran.

Saudi Arabia, Turkey, Egypt, and Afghanistan are also said to be interested, along with other likely contenders for BRICS membership, which includes Kazakhstan, Nicaragua, Nigeria, Senegal, Thailand, and the United Arab Emirates. All of them had their finance ministers present at the BRICS Expansion Dialogue meeting held last May. And if they all joined, the expanded BRICS would have a nominal GDP 30% larger than the United States, represent over 50% of the world population, and control over 60% of global gas reserves.[i]

Following China’s diplomatic coup over the Middle East, President Macron of France and Ursula von der Leyen, President of the European Commission, visited President Xi in Beijing last week ostensibly to see if he could persuade the Russians to consider a peace deal over Ukraine. That got nowhere. But the Chinese appear to see France as a more important trade partner than the European Commission. While Macron got the full diplomatic treatment, von der Leyen who recently delivered a hawkish speech over Taiwan was side-lined.[ii]

Macron’s popularity with China’s leadership is undoubtedly connected with his longstanding policy of promoting diplomatic and trade relations between China and France, with China making substantial investments in France. And it was recently announced that a French exporter of LNG to China even accepted payment in renminbi instead of dollars.

Clearly, the Chinese took all this into account in fêting Macron. Furthermore, Macron told journalists on the flight from Beijing to Guangzhou that Europe must not be a follower of the US agenda regarding Taiwan, and that European nations should not become entangled in “crises that are not ours” (Daily Telegraph, 11 April). Subsequently, Macron’s press office sparked a row by trying to censor his earlier comments.

This episode suggests that France is distancing itself from EU unity over foreign policy, and one wonders how little it might take to fracture not just the official EU approach, which is more in line with von der Leyen’s position, but NATO as well. And we can guess at what Xi told Macron over Ukraine: stand up for yourselves as Europeans and do not act as American stooges. Then the Russians might talk but without the Americans at the table. Doubtless, this was the same message that Putin told Macron when he visited Moscow early last year.

Not only has China succeeded in securing diplomatic successes in the Middle East, but it has suddenly become the go-to hegemon for world affairs — hence Macron’s and von der Leyen’s visit. As well as BRICS, China is joint ringmaster for the Shanghai Cooperation Organisation. While her own economy’s GDP is second only to that of the United States in nominal terms ($14.7 trillion compared with $20.89 trillion) on a PPP basis China’s is significantly larger ($32 trillion against the US’s $23 trillion).[iii]

Furthermore, China is beginning to expand again with bank credit increasing, while bank credit in the United States is contracting. The signal sent to trade partners around the world is to align their interests with China rather than America. But the neutrals are also looking at the state of the fiat dollar based banking system, and most probably concluding that it presents systemic dangers which it would be wise to avoid.

The true position of the US banking system

The state of the US banking system is undoubtedly a cause for global concern. The days of low interest rates are now demonstrably over, and an assessment of the banking system’s survivability in a higher interest rate environment is surely being made by its foreign users. And it will not have escaped their notice that US money supply, which is mostly comprised of bank deposits, is contracting. The latest position for bank credit on the other side of their collective balance sheets is shown in the St Louis FRED graph below.

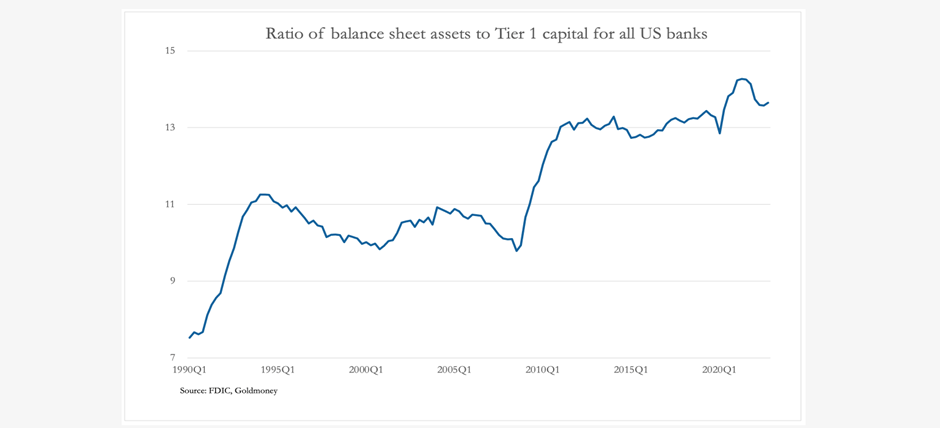

In percentage terms, bank credit has not yet declined as much as it did over the Lehman crisis, but it appears to be declining more aggressively. However, the common factors with every bank credit crisis are fear of losses replacing a desire for profits and their impact on highly leveraged bank balance sheets. The chart below, which is constructed from the FDIC’s bank ratio tables, illustrates the true position from a bank shareholder’s viewpoint.

As an approximation, we can see that based on the ratio of assets to Tier 1 capital that the entire banking system is significantly more leveraged than it has been since 1990, when the FDIC’s figures commenced.[iv] The ratio is now turning down, probably more so when 2023 Q1 statistics become available shortly.

Basically, there are two ways by which the ratio can return to more normal levels. Either banks raise more equity capital, which in many cases would be at a discount to book value and therefore undesirable. Alternatively, they must reduce the asset side of their balance sheets. Collectively, banks are choosing the latter course.

According to the FDIC, the reduction in total bank assets in 2022 was only $120bn, so banks had not addressed loan risk materially before January. But there were some important balance sheet trends. Securities Held declined $362bn, but within that total Available for Sale at Fair Value declined by $1,033bn while Held to Maturity increased by $676bn. Clearly, there was window dressing to conceal losses. $407bn in mortgage-backed securities were also sold. And cash balances were reduced by $981bn.

From the FDIC’s figures we can conclude that the reduction in bank credit last year was mostly of liquid assets instead of in the provision of credit for non-financial activities. Indeed, total loans and leases increased by $980bn. This means that over 2022, contracting bank credit reflected the banking system becoming less liquid, instead of containing risk. If anything, the risk from bank insolvency has thereby increased.

The Fed produces more up to date information than the FDIC’s. The features below are from the Fed’s H.8 table dated 7 April.

Overall, bank credit increased 1.6% year-on-year.All Securities in Bank Credit declined by 6% to $5,228.6bn. This includes Treasury and Agency Securities (down 4.7% to $4,153.4bn), Other Securities (down 11% to $1,075.2bn). Presumably, some of the fall is attributable to a rise in bond yields since last April, rather that actual bond selling. The true position is concealed by unknown quantities of bonds being reclassified to a held to maturity basis, rather than marked to market, as we saw with the Silicon Valley Bank failure.Loans and Leases in Bank Credit were up 5.1% on a year ago, but actually declined slightly compared with last month to $12,065.3bn. The Commercial and Industrial Loans subset declined by 5.4% to $2,756.1. We can assume that this figure represents revolving credit, and that so far it is too early to say that credit is being actively withdrawn from non-financial business activities.Consumer Loans continue to increase by 6.6%, but the figures are not large enough to be material for balance sheet totals.Cash Assets have fallen by 34% to $3,355.2bn. This line item represents vault cash, cash items in the course of collection, balances due from other banks, and from the Fed. This is also reflected in the FDIC’s numbers.In Liabilities, Large Time Deposits are up 43.9% to $1,843.9bn, but this is relatively small compared with the drop in Other Deposits, which have declined by $1,384bn since February 2022. With the fall in the Cash Asset line on the asset side, it signifies a significant decline in overall liquidity, both practically and from a regulatory viewpoint.

This leads us focus on the change in liquidity over the last year. Taking the change in Cash Items, the change in Other Deposits, and subtracting the increase in Large Deposits which are regarded as unstable funding, implies a total deterioration of $2,192bn. All these figures are seasonally adjusted, which taken over a year are not materially different from the actual. But in assessing the backing for the asset side of the banking system’s collective balance sheet, we must use non-adjusted numbers.

We see that while total assets have risen over the year by $523bn, residual assets less liabilities declined by $35.7bn to $2,158.6bn to give a ratio of the banking system’s total assets to its notional capital of 10.7 times. But on a proper risk-based capital ratio of 13.65 times based on the FDIC’s numbers in the second chart above, equity backing falls to $1,692 — scary in the context of losses that may arise in the coming months.

While at 13.65 times this ratio is excessively high compared with the past, it is less than banking ratios in other jurisdictions. And coupled with this high leverage, it is the deterioration of balance sheet liquidity which is concerning.

Derivatives are the elephant in the room

Many years ago, I was told by a successful company doctor that he was no longer in that line of work because he didn’t trust anyone’s accounts, management or audited. It is a sensible caveat to apply to our analysis of the US banking system when using publicly available information.

We know that stress tests of the banking system are designed to succeed, because no regulator will sign off on documents which confirm its own failure. It is less about quantifying system-wide risk of bank insolvency, and more about providing the wider public with a feeling of security.

Banks are dealers in credit, and much of their business is matching deposit obligations which can be withdrawn at little or no notice with assets which cannot be readily realised. This is why liquidity, or the ability to meet deposit withdrawals is so important. And this is why the deterioration in liquidity noted in our analysis is a warning signal.

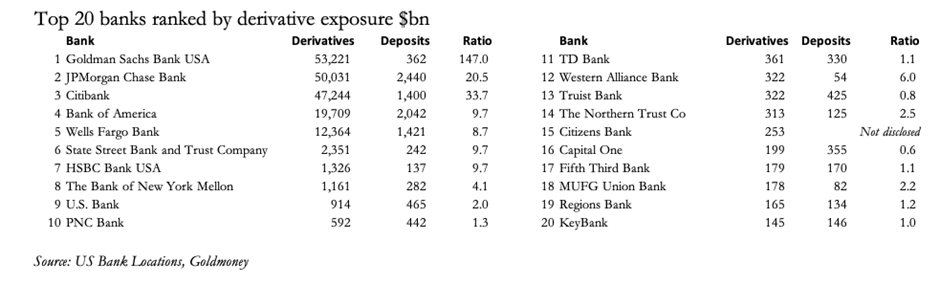

Furthermore, the fact that banks’ accounts are prepared in accordance with the approval of regulators means that they should still be treated with scepticism. For example, why is it that derivative obligations are not properly accounted for in assessing the condition of individual banks, when repos, which are similar obligations, are? Derivative obligations are far larger for some banks than the entire balance sheets of the combined banking systems, and even national GDPs. The table below show the derivative exposure of the twenty most exposed US banks, and the ratio of derivatives to customer deposits, which are the principal source of balance sheet funding.

Admittedly, not all derivative risk should be measured by their notional amount. Credit default swaps, which are likely to predominate in domestic banking activities, do not commit participants to settling their notional amounts, which are reference values only. But foreign exchange forwards and swaps and commodity derivatives as well as sold options do expose banks and other participants to settling their full amounts. Foreign exchange dollar exposure for US banks alone was estimated in a recent BIS paper at $80+ trillion, four times US GDP, and which included the following commentary:

“Embedded in the foreign exchange (FX) market is huge, unseen dollar borrowing. In an FX swap, for instance, a Dutch pension fund or Japanese insurer borrows dollars and lends euro or yen in the “spot leg”, and later repays the dollars and receives euro or yen in the “forward leg”. Thus, an FX swap, along with its close cousin, a currency swap, resembles a repurchase agreement, or repo, with a currency rather than a security as “collateral”. Unlike repo, the payment obligations from these instruments are recorded off-balance sheet, in a blind spot. The $80 trillion-plus in outstanding obligations to pay US dollars in FX swaps/forwards and currency swaps, mostly very short-term, exceeds the stocks of dollar Treasury bills, repo and commercial paper combined. The churn of deals approached $5 trillion per day in April 2022, two thirds of daily global FX turnover.”

BIS Quarterly review, December 2022

The BIS article goes on to point out that FX swap markets are vulnerable to funding squeezes, and that non-US banks owed $39 trillion in dollars from OTC derivatives, binding the US banking system into exceedingly high global systemic risk.

Commodity derivatives are similar to foreign exchange positions, and US banks are also active in these markets, both in regulated futures and OTC derivatives. The risks inherent in derivatives are considerably greater than mere contract failure, with chains of counterparties usually involved in OTC markets, spreading systemic risk from all financial centres into the US banking system and vice-versa. The proper inclusion of these liabilities on bank balance sheets on a gross basis (as opposed to a netted balance) not only blows a hole in the regulatory regime but would alert the public to the true leverage and therefore the risks to the banking system. Little wonder that these liabilities are hidden from public view.

Dealing with the fall-out from credit contraction

Contracting credit and the effect on interest rates have obvious consequences for individual borrowers. Furthermore, economic actors throughout the entire US economy have adapted their behaviour to benefit from heavily suppressed interest rates and the ready availability of credit under the assumption that these conditions will continue. Very few businessmen and consumers understood that they were in a credit bubble, which since interest rates began to rise is beginning to implode. We have witnessed the initial effects on bonds and financial assets, which take their valuation cue from the interest rate outlook. For now, the bubble implosion has paused, as energy prices declined from their peaks and the initial sense of panic has receded. But even without further credit contraction, we can see that the consequences of a readjustment to less free credit conditions are undermining the economies of the western alliance, which are now expected to enter a recession.

The dangers facing some non-financial sectors are already being flagged. For example, according to the Fed’s H.8 form Real Estate Loans increased over a year ago by $555bn to $5,385bn. At a time of rising interest rates and with hindsight, why the collective banking system increased its lending to this sector is difficult to justify. Will banks now see the error of doing so? At what point will they understand that the widespread contraction of credit undermines collateral values to the detriment of both the bank and its borrowers?

The answer to this and similar riddles is that there is a gradual dawning on us all of the consequences of banks becoming increasingly risk averse.

As interest rates begin to properly reflect the conditions of contracting credit, credit for private and commercial real estate will be withdrawn. Not only will financing costs rise, but the finance needed to maintain asset values will become unavailable. And the withdrawal of bank credit will also spread the crisis into commercial mortgage backed securities and other asset backed securities. It is the regional and smaller banks which are most exposed to this risk, and already there is growing speculation over the potential for a crisis in the commercial property sector.[v]

Consequences for foreign investors

So far, we have noted that foreign holders of dollars have been alerted to the fragility of the dollar-based banking system, and that access to their deposits and investments depends on the permissions of the United States, its five-eyes security network, and Western Europe’s NATO members. And they will also be thinking ahead about how the Fed, the ECB, and other major central banks will respond if the banking position deteriorates further. They will be posing the following what-ifs:

What if interest rates tend to rise further, driven by contracting credit availability instead of central bank monetary policies? Will that lead to more bank failures as the credit needed to support the mountain of derivatives dries up?What if the US and its allies face a recession? How will that affect the dollar and other currencies, compared with China’s renminbi, and whose economy is growing?What if China and Russia between them come up with sounder monetary alternatives to the dollar-based currency system? What will be the impact on the dollar and its purchasing power for commodities and their derived products?

Central to understanding these outcomes will be to anticipate the response by the relevant monetary authorities to contracting bank credit. Because GDP is almost all settled by transfers of bank credit, a reduction in its quantity automatically leads to a decline in nominal GDP. The consequences expected will be a rise in unemployment, a decline in government revenues, and an increase in welfare costs. In other words, government deficits will increase and so will their borrowing requirements.

This would place the US and its dollar in an awkward position. In recent decades, the US has become increasingly reliant on foreign buying of US Treasury debt, but since the dollar was weaponised against Russia that source of funding is declining. Indeed, in the year to January, foreign holders reduced their holdings by $253bn. And within that total non-government holdings increased by $163bn, while foreign governments reduced theirs by $416bn.

The valuation of these holdings would be undermined by contracting bank credit, because unless credit demand falls more rapidly than its supply, interest rates and bond yields will be driven higher by a credit shortage. Under these circumstances, a government is faced with having to issue bonds at higher yields in order to fund its deficit, irrespective of its central bank’s monetary policy. And as the UK found in its multiple funding crises in the 1970s, faced with this situation foreign holders of both bonds and a currency turn sellers.

This may seem obvious to a foreign holder of US assets and the dollar. Already primed to reduce their exposure to weaponised dollars in favour of China’s renminbi, foreign selling of dollars (and perhaps less obviously as well of euros, sterling, and yen which similarly face a combination of contracting bank credit, rising interest rates, commercial bank insolvency, and even central bank insolvency) it would appear that the days of holding reserve currencies headed by the dollar could come to an end. Foreign liquidation of the western alliance’s currencies and bonds will then clash with escalating funding requirements due to the consequences of recession on their governments’ finances.

From our analysis of deteriorating liquidity and high leverage in the US banking system — not so leveraged as the allied banking systems in Europe and Japan — it is clear that the banking crisis is in its earliest stages. Furthermore, the off-balance sheet nature of derivative obligations and the on-balance sheet losses hidden by sympathetic accounting regulations suggest that central banks will have to stand behind their commercial banking systems in their entirety. Attempts to impose the discipline of moral hazard selectively will almost certainly backfire.

But having also acquired bonds and other assets through quantitative easing at the highest possible prices, central banks themselves are only solvent by either recapitalising at the worst possible time, or by expanding their currency obligations by unimaginable quantities.

The developed world faces a perfect storm, seemingly certain to destroy its fiat currencies. By way of contrast, China and Russia between them have a credible plan for the industrial expansion of Asia. Both governments’ finances are stable, with China’s banking system savings-driven instead of the consumer-driven alternative in the west. This means that consumer prices in turn are stable, and the renminbi has the desirable characteristics of a relatively strong currency.

Furthermore, the mood music coming out of Russia is that they are considering returning the rouble to a gold standard. And failing that or even in addition to it, they are working on a separate gold or commodity backed currency for commodity pricing and trade settlement purposes. There are obvious benefits of such a move. Interest rates and rouble-denominated bond yields will decline over time from current levels of 10%, to a stable 2%–3% base level. And not only will volatility in energy and commodity prices be substantially reduced for the obvious benefit of financing production, but the unstable dollar will be banished from their trade — a long-standing ambition for both Russia and China.

It is hardly surprising therefore, that the non-aligned world is gravitating away from dollars and euros to renminbi and other currencies.

Price inflation in western economies will not decline to target

Macroeconomists expect falls in prices due to a slump in demand: in other words, they anticipate a surplus of production — a Malthusian glut. There might be a negative price effect from inventory liquidation, but that is only a short-term effect and does not set the subsequent course for the general price level, which is reflected in the value of a unstable fiat currency measured by a general price level.

The expected slump in demand as a recession progresses is assumed to be because unemployment rises, and therefore increasing numbers of unemployed consumers will have less to spend. Undoubtedly this is true. But at the same time, production declines. And while the balance of supply and demand will vary for different goods and services, in some cases product output will even decline more rapidly than demand for it. Therefore, it can never be said that a recession leads to a general surplus. Indeed, Say’s law, which was traduced by Keynes to pave the way for his state-directed economic theories, is clear on the matter.

While production still funds consumption through the medium of money and credit and a general balance between them is maintained, it is the value of commodities which appears likely to lead to price declines, because the onset of a recession can be expected to lead to a commodity surplus, before extractive industries respond by cutting their output. Measured in fiat currencies, oil and gas prices are particularly volatile. But the relationship is not so straightforward.

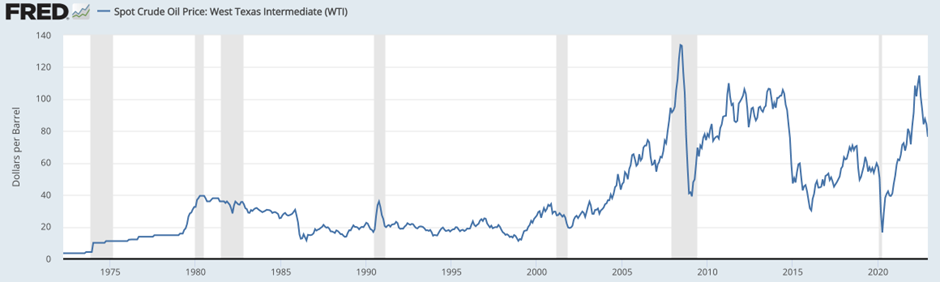

The chart below shows the price of WTI oil in US dollars and officially designated recessions, which are shaded. The correlation between the two is unclear, with the oil price rising early in the designated recessions in 1990 and 2007, while it fell sharply ahead of the brief recession in 2020. But it did fall after the recessions in 1991, 2001, and 2008 were well underway. Where there is a correlation, the price effects of recessions on oil and other commodities were probably exaggerated by speculative activity in derivatives, which even drove front-end WTI prices briefly into negative territory in April 2020.

There are also price changes emanating from changes in the currency’s valuation. WTI oil prices rose from below zero in April 2020 to a peak at $120 in only twenty-three months. But even before the Russians invaded Ukraine, while it was widely expected that they would not invade the price had risen to $90.

Therefore, as banks tighten credit conditions and the western alliance’s economies drift towards recession, the general level of consumer prices will not slump as commonly forecast by official bodies, and consequently changes in the general level of prices will predominantly reflect changes in their respective fiat currencies’ purchasing power.

The macroeconomic fallacy predicting a general glut is behind an IMF report this week which forecast interest rates in the UK returning to “ultra-low levels”. Or rather, that was the media report on Chapter 2 of the IMF’s World Economic Outlook, which was trying to assess the (mythical) natural rate of interest on the assumption that price inflation would return to target. You could put money on it being wrong. No amount of mathematical modelling can capture variations in the level of human confidence in a currency, and therefore the compensation depositors will require to lend expanded credit in it.

Conclusion

All the signs point to a termination of the world’s fiat currency regime. And with it, there will be a radical change in central banking. Given that central banks in the western alliance are all technically bankrupt themselves, their survivability and that of their currencies is questionable.

Out with the fiat currency system will go the SDR and central bank currency reserves. Only credible gold backing for currencies will guarantee their value measured by the general level of prices. It will create considerable hardship for the 1.3 billion people in North America, Europe, Japan, and the antipodes. Against that, the 3.8 billion in Asia, as well as a further billion in Africa, and most of the balance of global humanity will have the opportunity of a better life.

The extent to which those of us inhabiting the world of yesteryear suffer will depend on how long it takes for our statist establishments to recognise their policy errors, the practical limitations of the state, and to persuade its electors that freeloaders cannot be the state’s responsibility. The entire science of macroeconomics has led us into a state of delusion and must be abandoned. Free markets must be embraced again, and the state minimised.

The way to respond to the Asian hegemons is to encourage free trade and do away with trade tariffs as much as possible for the mutual benefit of all nations. We must mimic their foreign policies, which are to recognise other governments and cultures, only intervening to protect our direct interests. This was the wisdom of Lord Liverpool, Castlereagh, and Wellington in charting a course for Britain following the Napoleonic Wars, setting the course for Britain to become the most powerful economic force in the nineteenth century.

But where we can have something superior to them is in a respect for property rights because that is the one great flaw in both Russia and China, where state interests use the law or main force to deprive citizens of their property and freedom.

Meanwhile, it makes sense for us as individuals to get out of a failing fiat currency financial system and hoard legal money in defence of what wealth we have. And that is gold.

[i] See Silk Road Briefing: https://www.silkroadbriefing.com/news/2022/11/09/the-new-candidate-countries-for-brics-expansion/ [ii] Politico reported on this here: https://www.politico.eu/article/china-divide-rule-eu-france-unity-ursula-von-der-leyen-emmanuel-macron-xi-jinping/ g [iii] See World Economics: https://www.worldeconomics.com/Indicator-Data/Economic-Size/Revaluation-of-GDP.aspx [iv] See the FDIC’s spreadsheet on Ratios by asset size group. The chart is for all insured institutions. https://www.fdic.gov/analysis/quarterly-banking-profile/index.html [v] See this from Moody’s: https://cre.moodysanalytics.com/insights/cre-news/whats-the-real-situation-with-cre-and-banks-doom-loop-or-headline-hype/Source link